Suvarn

Statistics-Based Quantitative Analysis Engine

What it is

Suvarn is a quantitative research project focused on developing and evaluating statistical models for financial markets- More specifically, the Indian financial markets. The emphasis is on robustness, traceability, and adaptability to different market regimes.

Why I'm building it

I built Suvarn to study how theoretical models like Bayesian modelling, Kalman state spaces and regression analysis etc interact and predict(or try to) real instruments. The project taught me to confront and avoid issues like data leakage and overfitting, and also gave me experience working with transformers trained for regression analysis.

How it works(High-Level)

At a conceptual level, Suvarn uses both technical analysis and fundamentals to generate daily/weekly signals.

Sentiment analysis unit collects data from news sites and social media platforms like reddit to generate sentiment scores per stock.

Technical analysis unit combines kalman state modelling, bayesian modelling, and state space graphs to generate technical strength scores for each ticker.

A final aggregation layer combines technical and sentiment signals into a unified assessment.

Risk aware evaluation metrics and stress tests including but not limited to monte-carlo simulations.

Evidence and gallery

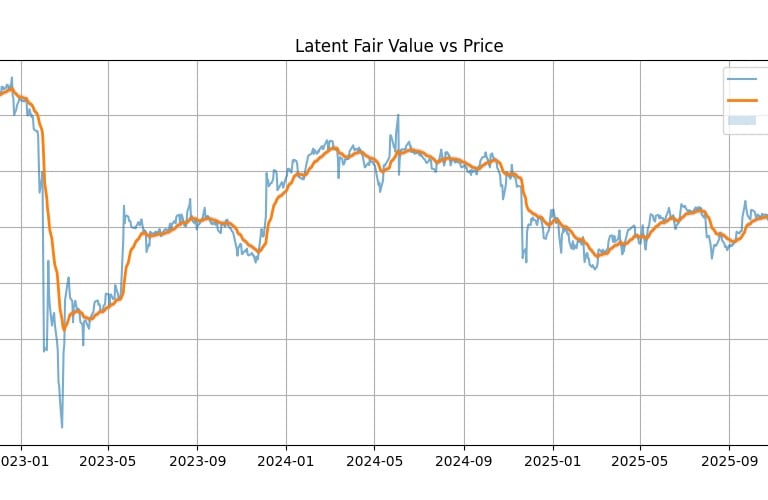

Fair Value Indication

Alpha gained from runs of overpricing.

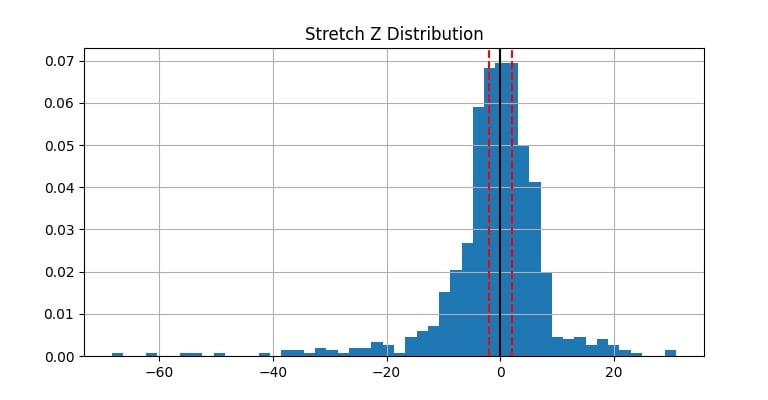

"Stretch-Z"

Normalized Z-Score indication.

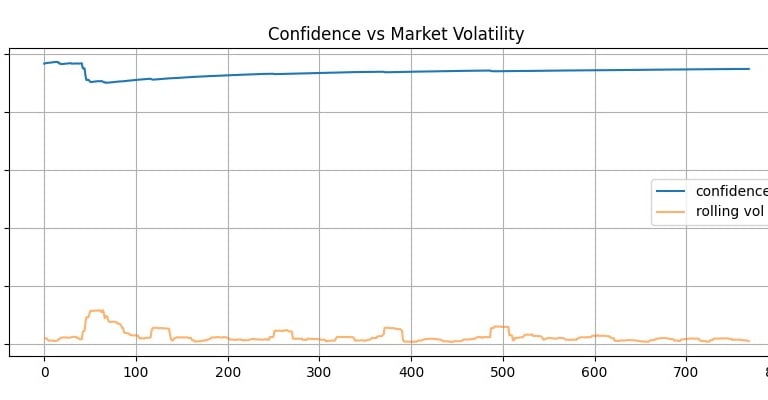

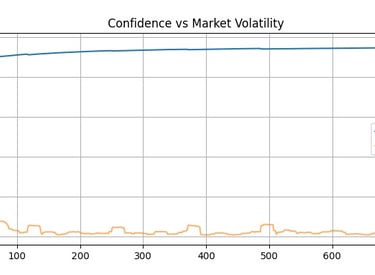

Confidence V Volatility

Market sentiment vs Volatility to ensure selecting only high Sharpe stocks.

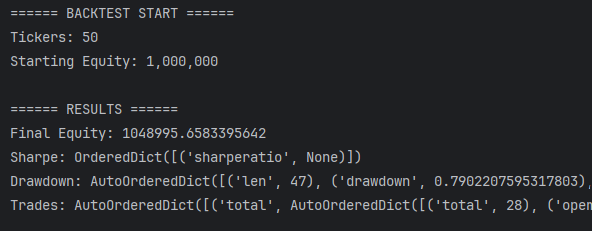

Example backtest

Illustrative backtest demonstrating signal behavior and risk evaluation methodology. Numerical values are intentionally anonymized to emphasize model behavior over performance.